Software as a Medical Device is redefining medical technology, beginning with AI-driven CT reconstruction that reduces scan time, radiation, and cost. With a global market exceeding USD 10 billion, SaMD is expanding into diagnostics, therapeutics, and decision support, fundamentally shifting devices from hardware-centric tools to continuously learning, software-led clinical systems.

This year, I had a medical check-up as part of an annual check at NURA. The lab where I had taken the test had scheduled the checkup for 2 hours, and that included a CT scan. While doing the scan, my exposure time was less than 8 minutes, for a CT scan to check for blockages. What was interesting was that the CT scan in use was developed by Fuji, which has advanced AI and Fujifilm technology to provide high-quality, detailed health screenings with significantly less radiation (up to 97% less than standard CTs) for early detection of cancers, heart issues, and organ problems. This is enabled by AI and SaMD.

The SaMD market is growing exponentially globally, and while the use case I have explained above is one of the many advantages, there seems to be renewed interest in this market, specifically in countries like India. The Indian government just released their guidelines on SaMD. There is optimism that this will change the future of the medical devices market, specifically in critical areas like diagnostics and imaging, where the hardware requirements make the devices very capex heavy, requiring significant investment.

Software as a Medical Device (SaMD) has moved from experimentation to scaled clinical deployment, driven by AI maturity, regulatory clarity, and hospital demand for productivity gains. The market is consolidating around a few dominant players while opening space for niche, indication-specific innovators.

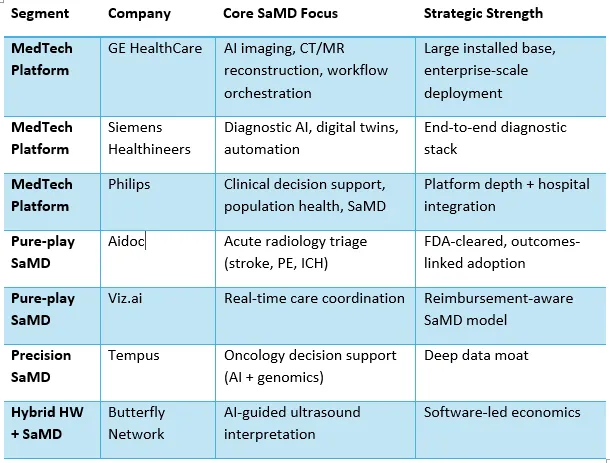

At first glace it looks as if traditional hardware-based medical device companies have an advantage and will dominate the market. That is indeed correct and later I will explain why they have an advantage as we switch from a hardware-only to a hardware + SaMD construct. Closely following them are the pure play SaMD providers, they have superior technology and better algorithms, but is that enough to win in the healthcare market? We will come to that question later, and the answer is linked to my statement above on the hardware players.

Some interesting hybrid entities have emerged, which look at a combination, but it is in a narrow therapeutic area. While it is yet to move beyond Ultrasound, this is an interesting development, and we should watch this space with interest. Then there are players in the precision category that look at specific therapeutic areas. Much more interesting and given the growth in single speciality healthcare enterprises this will add more value in the coming days. This space is already full of other software that is integrated.

Below are the key market shifts that I am seeing that will make the SaMD market more strategic, and these I see playing out from now till the end of 2029.

SaMD began as narrow algorithms solving isolated problems—such as AI-based CT reconstruction, reducing scan time and radiation exposure. The market is now consolidating toward platform-based SaMD, where multiple algorithms operate across the diagnostic and clinical workflow. Hospitals increasingly prefer vendors who can scale across departments rather than manage fragmented AI tools. This favours incumbents and well-capitalised pure plays that can orchestrate multiple clinical use cases within a single software ecosystem. That’s why the traditional players have an advantage and answer the question of why they are most likely to do well in the SaMD construct.

A critical inflection point for SaMD has been regulatory clarity. FDA’s SaMD guidance, EU MDR frameworks, and IMDRF alignment have reduced uncertainty for developers and investors. Importantly, regulators are now engaging with concepts such as adaptive and continuously learning algorithms, which were previously a bottleneck for AI-led SaMD. This maturation is shifting SaMD from pilot-stage deployments to enterprise procurement and long-term clinical contracts. As mentioned earlier, even India has released its guidelines for SaMD, sparking a new interest in this area.

Clinical accuracy is no longer sufficient. Health systems now demand economic outcomes, reduced scan times, faster clinical decisions, lower length of stay, and avoidance of adverse events. SaMD procurement committees increasingly evaluate tools on operational ROI and reimbursement alignment rather than sensitivity and specificity alone. This is driving SaMD vendors to publish real-world evidence, not just validation studies, and to align pricing with measurable value creation. At the end of the day at investment made in technology, including AI has to stem from how closely they are aligned to the KPIs of the healthcare system. This point alone is the key reason why pureplay AI has not scaled in healthcare.

SaMD adoption is highest when software integrates seamlessly into existing clinical workflows, PACS, RIS, EHRs, and clinical communication platforms. Standalone AI dashboards have consistently underperformed. The winners are SaMD products that are invisible to clinicians yet influential in decision-making. This explains why vendors with deep hospital integration capabilities outperform technically superior but workflow-agnostic competitors. This is the key reason why I feel the pureplay will have to work on enhancing its knowledge of the hospital workflows. Algorithm superiority will mean very little if the outcomes are not immediate, and the user experience for clinicians is much superior to what is available today.

The next phase of SaMD growth is shifting beyond diagnostics into therapeutic and autonomous domains—AI-driven dosing, closed-loop monitoring, digital therapeutics, and interventional guidance. This transition materially increases clinical risk, regulatory scrutiny, and value creation. Therapeutic SaMD will redefine the medical device paradigm, where software, not hardware, becomes the primary clinical actuator.

SaMD is no longer an adjunct to medical devices it is becoming the core logic layer of care delivery. I will challenge one implicit assumption: the future winners will not be the best algorithms, but the best integrators of regulation, workflow, and economics. This alone will determine who wins this new platform-driven, integrated healthcare system, well-orchestrated by SaMD.

Dr. Vikram Venkateswaran is a healthcare strategist, clinician, and innovator with over 25 years of experience spanning clinical practice, digital health, automation, and healthcare transformation in India. He is the founder of Healthcare India and the author of Own Your Health. Dr. Venkateswaran advises, invests in, and builds technology-led healthcare platforms. He is based in Bengaluru.